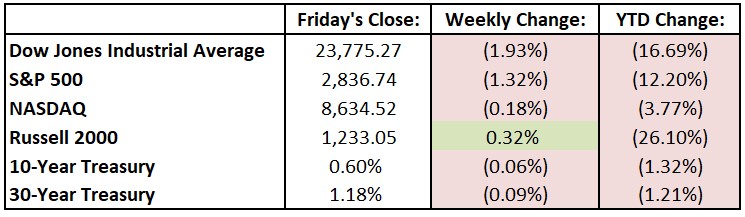

Last Week’s Highlights:

Stocks and bonds fell sharply early in the week as oil futures crashed, then roared back after another stimulus bill was announced. Earnings season for U.S. companies continued, and more weak economic numbers were released – it was reported that an additional 4.4 million Americans are seeking jobless benefits. For the week, the Dow Jones Industrial Average (DJIA) dropped 467.22 points, or 1.9%, to 23,775.27, while the S&P 500 was down 1.3% to 2836.74 and finished 23% above its March low. The tech-heavy NASDAQ declined 0.2%, closing at 8634.52. Late last week, the World Health Organization accidently released what appeared to be disappointing results from a trial of Gilead Sciences’ (GILD) remdesivir, a potential treatment for COVID-19. While this release caused a 400+ point drop in the Dow on Thursday, the index roared back Friday to close up 260 points, or 1.11% on the day.

Looking Ahead:

We’re in the thick of first-quarter earnings season – 142 S&P 500 components release results this week, followed by a similar number next week. The week begins with financial results from CMS Energy (CMS) and NXP Semiconductors (NXPI) on Monday. Tuesday is a busy one for more earnings, as 3M (MMM), Caterpillar (CAT), Mondelez International (MDLZ) and United Parcel Service (UPS) are among a bevy of companies reporting. The Bank of Japan announces its monetary-policy decision – the central bank is expected to keep its key short-term interest rate at negative 0.1%. Wednesday brings financial results from Anthem (ANTM), Automatic Data Procession (ADP), General Electric (GE) and Northrop Grumman (NOC). The Bureau of Economic Analysis reports its initial estimate of GDP for the first quarter – economists forecast an annualized 4% contraction, compared with a 2.1% growth rate in the fourth quarter of 2019. Altria Group (MO), Apple (APPL), Visa (V) and Comcast (CMCSA) are among the many companies reporting numbers on Thursday. The busy business week ends with results from Chevron (CVX), Honeywell International (HON), Colgate-Palmolive (CL) and Charter Communications (CHTR) on Friday. The Institute for Supply Management reports its Manufacturing Purchasing Managers’ Index for April – expectations are for a 36.1 reading, down from March’s 49.1 print.

All of us at Tufton Capital wish you a safe and healthy week!

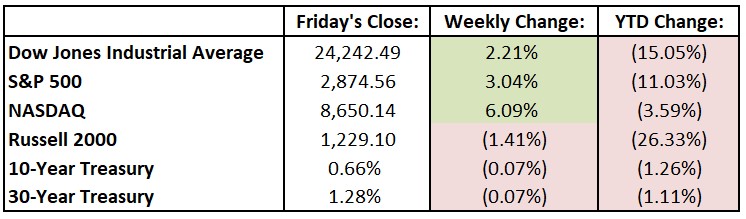

Last Week’s Highlights:

Equities rose for the second week in a row, extending a solid rally despite evidence of increasing economic strain due to the coronavirus pandemic. The stock market’s recent strength is a sign that many investors are positioning their portfolios believing that the U.S. will make a speedy recovery when the coronavirus crises eases. Wall Street has been encouraged in recent days by signs that several states will move to resume business, along with hopes that a viable treatment for Covid-19 could be near. For the week, the Dow Jones Industrial Average (DJIA) rose 523.12 points, or 2.2%, to 24,242.49, while the S&P 500 was up 3.0% to 2874.56 and finished 22% off its March low. The tech-heavy NASDAQ increased 6.1%, closing at 8650.14. Earnings season began last week with mixed results. Management teams from JP Morgan Chase (JPM) and Wells Fargo (WFC) predicted a deep recession, and data from oil companies and retailers was, as expected, weak. On a brighter note, an upbeat early report on Gilead Science’s (GILD) Covid-19 treatment added to a significant stock rally on Friday.

Looking Ahead:

Earnings season picks up, beginning with reports from Cadence Design Systems (CDNS), Equifax (EFX), Halliburton (HAL) and Truist Financial (TFC) on Monday. The Federal Reserve Bank of Chicago releases its National Activity Index for March – economists forecast a minus 0.56 reading, below February’s 0.16 print. Chipotle Mexican Grill (CMG), Chubb (CB), Coca-Cola (KO), Emerson Electric (EMR) and Lockheed Martin (LMT) all report financial results on Tuesday. The National Association of Realtors releases existing-home sales data for March – consensus estimates are for a seasonally adjusted annual rate of 5.47 million homes sold, 5.2% below February’s 5.77 million figure. Wednesday brings earnings results from AT&T (T), Biogen (BIIB) and Delta Air Lines (DAL). Capital One Financial (COF), Intel (INTC), Union Pacific (UNP) and Eli Lilly (LLY) announce financial results on Thursday. The Department of Labor releases its initial jobless claims for the week ending on April 18th – over the past month, 22 million people have applied for unemployment benefits, roughly double the total in all of 2019. American Express (AXP) and Verizon Communications (VZ) hold conference calls on Friday to discuss quarterly results. The Census Bureau reports the durable goods number for March – consensus estimates are for a 11% decline in orders for manufactured durable goods.

All of us at Tufton Capital wish you a safe and healthy week!

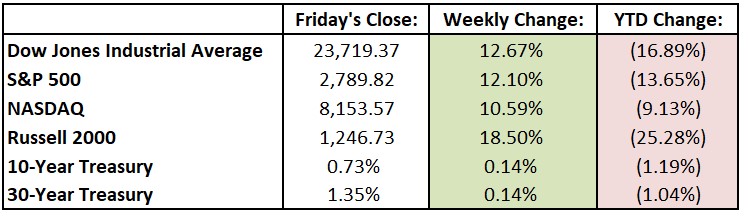

Last Week’s Highlights:

Equities rose to post one of their biggest weeks of gains, extending a solid rally despite evidence of increasing economic strain due to the coronavirus pandemic. Last week’s dismal jobless claims report (an additional 6.6 million claims were reported) was overshadowed by the Federal Reserve’s announcement of more lending backup. Oil prices surged as OPEC appeared to agree on cutting 10 million barrels a day in output. For the week, the Dow Jones Industrial Average (DJIA) rallied 2666.84 points, or 12.7%, to 23,719.37, while the S&P 500 rose 12.1% to 2789.82 – its best week since 1974 – and finished 25% off its March low. The tech-heavy NASDAQ increased 10.6%, closing at 8153.58.

Looking Ahead:

Many bourses are closed around the world on Monday, including Germany and the United Kingdom, in observance of Easter. Fastenal (FAST), J.B. Hunt Transport Services (JBHT) and Johnson & Johnson (JNJ) report earnings results on Tuesday. The International Monetary Fund releases its April 2020 World Economic Outlook – the IMF’s previous update in January forecasted global gross-domestic-product growth of 3.3% and 3.4% in 2020 and 2021, respectively. Wednesday brings financial results from Bank of America (BAC), Goldman Sachs Group (GS), UnitedHealth Group (UNH) and U.S. Bancorp (USB). The Federal Reserve Bank of New York releases its Empire State Manufacturing Survey for April – expectations call for a minus 32 reading, down from March’s minus 21.5 print. Abbott Laboratories (ABT), Bank of New York Mellon (BK) and Taiwan Semiconductor Manufacturing (TSM) hold conference calls on Thursday to discuss earnings results. The Department of Labor releases initial jobless claims for the week ending on April 11th – over the past three weeks, an unprecedented 16.7 million people have filed unemployment claims. Kansas City Southern (KSU) and State Street (STT) report quarterly results on Friday.

All of us at Tufton Capital wish you a safe and healthy week!

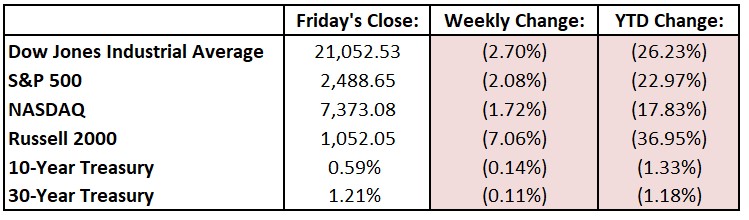

Last Week’s Highlights:

Equities declined last week amid soft economic data and the extension of social-distancing guidelines. Thursday’s jobless claims report exceeded 6.6 million, twice the week-earlier record high. Oil prices surged 32% on prospects of a global deal to cut output and support prices. For the week, the Dow Jones Industrial Average (DJIA) fell 584.25 points, or 2.7%, to 21,052.53, while the S&P 500 dropped 2.1% to 2488.65. The tech-heavy NASDAQ declined 1.7%, closing at 7373.08. Volatility continued in the markets, although at a lower level than investors have experienced in past weeks. The CBOE Volatility Index (or VIX) tumbled 29% last week, finishing below 50 for the first time since early March. While the VIX still trades at an elevated level, it’s far below the 70s and 80s levels seen in recent weeks. New York remained the epicenter of the Covid-19 crisis, with cases and deaths mounting as it neared its apex. Meanwhile, new clusters erupted across the U.S. – Louisiana, Florida, Georgia and Texas – as more states moved to shelter-at-home policies and governors pleaded for medical equipment from the federal government.

Looking Ahead:

Stock futures rallied Sunday night, a hopeful sign as Wall Street begins another unprecedented week of trading. On Monday, the Saudi Arabia-led Organization of Petroleum Exporting Countries (OPEC) holds an emergency meeting with its non-OPEC allies, notably Russia, in an attempt to stabilize oil prices. Levi Strauss & Co. (LEVI) announces quarterly results on Tuesday. The Federal Reserve reports consumer credit data for February – last year, consumer borrowing climbed 4.5%, to nearly $4.2 trillion, still below the five-year average jump of 5.6%. Costco Wholesale (COST) releases sales data for March on Wednesday. Thursday brings annual shareholder meetings for Adobe (ADBE) and Dow (DOW). The University of Michigan reports its Consumer Sentiment Index for April – economists forecast a 79 reading, a large decline from March’s 89.1 print. On Friday, the Bureau of Labor Statistics (BLS) releases the consumer price index (CPI) for March – consensus estimates are for 1.3% rise year-over-year, after a 2.3% increase in February. Equity and fixed-income markets in the U.S. are closed in observance of Good Friday.

All of us at Tufton Capital wish you a safe and healthy week!

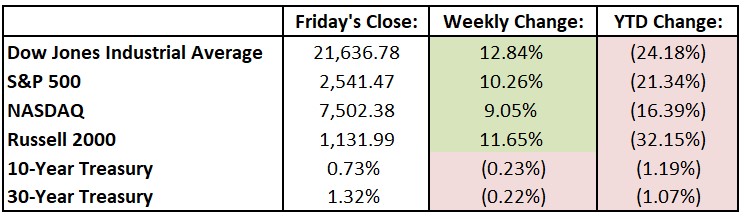

Last Week’s Highlights:

Fiscal and monetary policies helped lift equity markets, as the Dow Jones Industrial Average (DJIA) posted its biggest weekly gain since 1938. The Federal Reserve has dropped interest rates to near zero and is purchasing large quantities of Treasuries and other securities. Congress passed a $2 trillion spending package worth about 9% of U.S. gross domestic product. For the week, the Dow rallied 2462.80 points, or 12.8%, to 21,636.78, while the S&P 500 gained 10.3% to 2541.47. The tech-heavy NASDAQ rose 9.1%, closing at 7502.38. Even after last week’s market rally, equities are still down 25% from the peak reached a month ago. The coronavirus pandemic has forced widespread shutdowns and has ground much of the U.S. economy to a halt, and last week 3.28 million people filed for unemployment benefits, well above previous records.

Looking Ahead:

Global investors are preparing for another volatile ride this week. On Monday, the National Association of Realtors reports pending home sales for February – economists forecast a 1.3% decline, after a 5.2% jump in January. Broadcom (AVGO) hosts its annual shareholder meeting. Spice maker McCormick (MKC) and Conagra Brands (CAG) report quarterly results on Tuesday. The Institute for Supply Management (ISM) releases its Chicago Purchasing Managers’ Index for March – economists forecast a 39 reading, well below the expansionary level of 50. Wednesday brings earnings reports from Lamb Weston Holdings (LW) and PVH (PVH). Hewlett Packard Enterprise (HPE) and Schlumberger (SLB) hold their annual shareholder meetings. CarMax (KMX) and Walgreens Boots Alliance (WBA) announce financial results on Thursday. The Department of Labor reports initial jobless claims for the week ending on March 28th. Constellation Brands (STZ) holds a conference call on Friday to discuss quarterly earnings results. The ISM releases its Non-Manufacturing Index for March – economists look for a 45 reading, well below February’s 57.3 print.

All of us at Tufton Capital wish you a safe and healthy week!

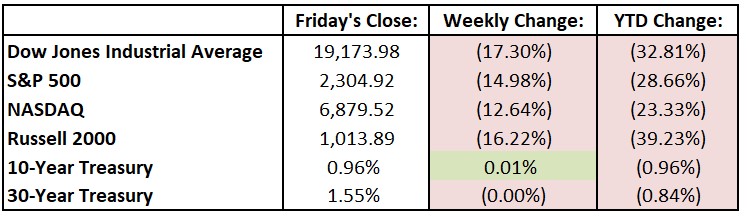

Last Week’s Highlights:

Equity markets finished sharply lower and volatility persisted as the number of coronavirus cases continued to rise globally. Central banks and governments around the globe rushed to announce support measures amid event cancellations, school closures and work-from-home arrangements. The U.S. called for a $1.2 trillion stimulus plan and European countries reported a combined $1 trillion in new fiscal spending. The Federal Reserve cut interest rates by a full percentage point and announced that it would buy $700 billion in Treasuries and mortgage-backed securities. For the week, the Dow Jones Industrial Average (DJIA) fell 4011 points, or 17.3%, to 19,173.98, while the S&P 500 dropped 15% to 2304.92. The tech-heavy NASDAQ lost 12.6%, closing at 6879.52. Stock market futures were weak Sunday night but appear to have recovered going into Monday morning on news of additional Fed stimulus.

Looking Ahead:

Global investors are preparing for another volatile ride following a week of frantic and at times disorderly trading. On Monday, the Federal Reserve Bank of Chicago releases its Chicago Fed National Activity Index for February – consensus estimates call for a -0.43 reading, in line with the January data. Nike (NKE) and IHS Markit (INFO) release quarterly results on Tuesday. The Census Bureau announces new residential home sales for February – economists expect a seasonally adjusted annual rate of 740,000 homes sold. Micron Technology (MU) and Paychex (PAYX) report earnings on Wednesday. The Federal Housing Finance Agency releases its Home Price Index for January. Thursday brings earnings announcements from GameStop (GME) and Lululemon Athletica (LULU). The Department of Labor reports initial jobless claims for the week ending on March 21st – expectations are for an annualized 2.1% rate of growth, unchanged from the second estimate released in late February. On Friday, the Bureau of Economic Analysis releases its Personal Income and Outlays report for February – personal income is expected to rise 0.3%, following a 0.6% jump in January.

All of us at Tufton Capital wish you a safe and healthy and week!

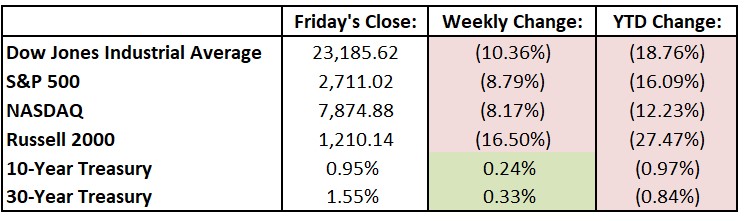

Last Week’s Highlights:

Equity markets finished sharply lower and entered into bear-market territory after the World Health Organization declared the coronavirus a global pandemic and oil prices saw the biggest one-day decline since 1991. Central banks and governments around the globe rushed to announce support measures amid event cancellations, school closures and work-from-home arrangements. For the week, the Dow fell 2,679 points, or 10.4%, to 23,185.62, while the S&P 500 dropped 8.8% to 2711.02. The tech-heavy NASDAQ lost 8.2%, closing at 7874.88. The week’s drop for the Dow Jones came despite an epic 1,985-point rally on Friday. The Federal Reserve took drastic emergency action Sunday evening to stabilize the economy. The Fed cut interest rates by a full percentage point and announced that it would buy $700 billion in Treasuries and mortgage-backed securities. Stock market futures were crushed Sunday night despite the Fed action (down over 4% – trading “limit down”), setting up what will be another very volatile week ahead on Wall Street.

Looking Ahead:

Global investors are preparing for another volatile ride following a week of frantic and at times disorderly trading. Monday brings earnings releases from Coupa Software (COUP) and Tencent Music Entertainment Group (TME). The Federal Reserve Bank of New York releases its Empire State Manufacturing Survey for March – consensus estimates call for a 0.5 reading, down from February’s 12.9 print. FedEx Corp. (FDX) announces financial results on Tuesday, and American Express (AXP) webcasts its 2020 Investor Day. Wednesday brings earnings from General Mills (GIS), and Agilent Technologies (A) and Starbucks (SBUX) host their annual shareholder meetings. The Census Bureau reports new residential construction data for February – economists look for a seasonally adjusted annual rate of 1.48 million housing starts, down from January’s 1.55 million. Accenture (ACN) and Darden Restaurants (DRI) report earnings on Thursday. The Conference Board releases its Leading Economic Index for February – consensus estimates are for a flat reading following a 0.8% gain in January. The National Association of Realtors reports existing-home sales for February on Friday – economists forecast a seasonally adjusted annual rate of 5.55 million homes sold, up 1.7% from January’s 5.46 million.

All of us at Tufton Capital wish you a good and safe week!

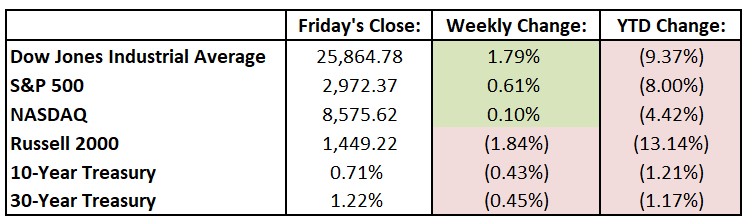

Last Week’s Highlights:

While it certainly didn’t feel like it, the three major U.S. stock market indexes posted modest gains last week following wild swings due to accelerating coronavirus fears and monetary stimulus hopes. (The Dow Jones Industrial Average (DJIA) was up 1293 (Monday), down 785 (Tuesday), up 1173 (Wednesday), down 969 (Thursday) and down 256 (Friday)). For the week, the Dow gained 455.42 points, or 1.8%, to 25,864.78, while the S&P 500 rose 0.6% to 2972.37. The tech-heavy NASDAQ advanced 0.1%, closing at 8575.62. By the end of the week, the yield on the 10-year U.S. Treasury note had fallen to 0.707%, its lowest on record. Stock market futures were crushed Sunday night (down over 4%), setting up what will be another very volatile week ahead on Wall Street.

Looking Ahead:

Global investors are preparing for another volatile ride following a week of frantic and at times disorderly trading. Monday brings earnings releases from Franco-Nevada (FNV) and Vail Resorts (MTN). Dick’s Sporting Goods (DKS) reports financial results on Tuesday. Qualcomm (QCOM) holds its annual shareholders meeting in San Diego. On Wednesday, the Treasury Department releases the U.S. monthly budget statement for February. For fiscal 2019, which ended in September, the federal deficit was $984 billion – the largest since 2012. The Congressional Budget Office projects a $1 trillion deficit for 2020. Thursday brings earnings reports from Adobe (ADBE), Broadcom (AVGO), Dollar General (DG) and Ulta Beauty (ULTA). The Bureau of Labor Statistics release the producer price index (PPI) for February – consensus estimates are for a flat reading, with the core PPI expected to rise 0.2%. Friday brings the University of Michigan’s release of its Consumer Sentiment index for March – economists forecast a 94 number, down from February’s 101 print.

The Tufton Capital Team hopes that you have a wonderful week!

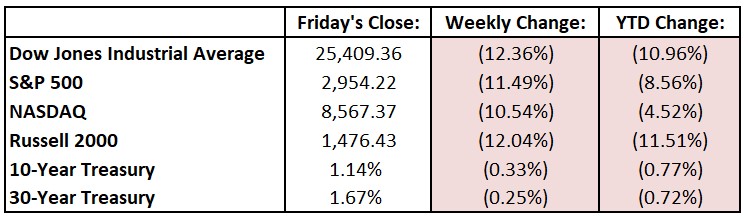

Last Week’s Highlights:

Equities plunged as the coronavirus spread beyond China. Pandemic fears shifted from China, where the outbreak began, to South Korea, Japan Italy and Iran. The United States reported its first case that couldn’t be traced overseas. Oil prices tumbled and “safe haven” assets soared – yields on 10-year Treasuries fell to record lows, and the yield-curve inverted. For the week the Dow Jones Industrial Average (DJIA) tumbled 3583.05 points, or 11.5%, to 25,409.36, while the S&P 500 fell 11.5% to 2954.22. The tech-heavy NASDAQ was down 10.5%, closing at 8567.37. Stock market futures were all over the place Sunday night, setting up what will be another very volatile week ahead on Wall Street.

Looking Ahead:

Global investors are preparing for another volatile ride following a week of frantic and at times disorderly trading. Monday brings earnings releases from Dentsply Sirona (XRAY) and Evergy (EVRG). The Census Bureau reports construction spending for January – consensus estimates call for a seasonally adjusted annual rate of $1.34 trillion, up 0.6% from December’s level. AutoZone (AZO), Nordstrom (JWN), Ross Stores (ROST) and Target (TGT) release financial results on Tuesday. It’s Super Tuesday in the Democratic primary, with a third of all delegates up for grabs as 14 states head to the polls. Wednesday brings earnings reports from Brown-Forman (BF), Campbell Soup (CPB) and Dollar Tree (DLTR). Exxon Mobil (XOM) webcasts its 2020 investor day on Thursday, and Burlington Stores (BURL), Kroger (KR) and H&R Block (HRB) report earnings. The Bureau of Labor Statistics (BLS) releases the jobs report for February on Friday – economists forecast a 175,000 rise in nonfarm payrolls and expect the unemployment rate to remain steady at 3.6%.

The Tufton Capital Team hopes that you have a wonderful week!

Last Week’s Highlights:

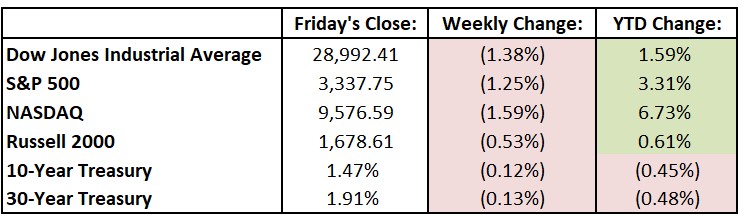

Equities sold off last week as investors flocked to traditionally safer assets such as government bonds and gold. The coronavirus epidemic and its impact on global growth continued to dominate headlines and will likely be the major international news story in weeks to come (more on this below). The yield on the benchmark 10-year U.S. Treasury note reached its lowest level since September on Friday, ending the day at 1.470%. For the week the Dow Jones Industrial Average (DJIA) dropped 405.67 points, or 1.4%, to 28,992.41, while the S&P 500 fell 1.2% to 3337.75. The tech-heavy NASDAQ was down 1.6%, closing at 9576.59. Merger mania continued, as Franklin Resources (BEN) agreed to buy Legg Mason (LM) for $4.5 billion, and Morgan Stanley (MS) announced a $13 billion all-stock deal for E*Trade (ETFC). Stock market futures dropped over 2% Sunday night as global worries about the coronavirus epidemic accelerated, setting up what will be a very volatile week ahead on Wall Street.

Looking Ahead:

A bevy of retailers will report financials this week, signifying the tail end of fourth-quarter earnings season. Japanese bourses are closed on Monday in observance of the emperor’s birthday. HP Inc. (HPQ), Intuit (INTU) and Palo Alto Networks (PANW) release quarterly results. JP Morgan Chase (JPM) hosts its 2020 investor day in New York on Tuesday. American Tower (AMT), Home Depot (HD), Macy’s (M) and Bank of Montreal (BMO) announce earnings results. Wednesday brings financials from L Brands (LB), TJX Companies (TJX) and Crown Castle International (CCI). The Census Bureau reports new residential home sales for January – expectations call for a seasonally adjusted annual rate of 710,000 single-family homes sold, up 2.3% from December. Best Buy (BBY), Dell Technologies (DELL) and Autodesk (ADSK) report numbers on Thursday. The Census Bureau releases the Durable Goods report for January – economists look for a 0.9% decline. The business week ends with earnings results from AES (AES) and Occidental Petroleum (OXY) on Friday. The Institute for Supply Management reports its Chicago Purchasing Manager’s Index for February – expectations are for a 45 reading, up from January’s 42.5 print.

The Tufton Capital Team hopes that you have a wonderful week!

Last Week’s Highlights:

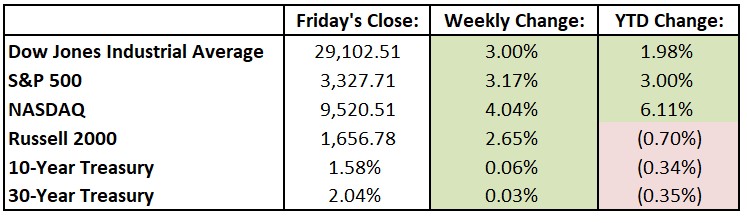

U.S. stocks posted their biggest weekly gains in months as concerns about a global economic slowdown due to the coronavirus eased. Equities hit new highs midweek before slipping on Friday, when the U.S. jobs report came in above expectations (225,000 jobs were added in January, beating the 165,000 estimate). Friday’s selloff is a classic case of good news is bad news, as the strong employment report may reduce the chance of a rate cut by the Federal Reserve in the coming months. For the week the Dow Jones Industrial Average (DJIA) rallied 846.48 points, or 3.0%, to 29,102.51, while the S&P 500 advanced 3.2% to 3327.71. The tech-heavy NASDAQ was up 4.0%, closing at 9520.51. Stocks taking center stage included Tesla (TSLA), which continued its volatile ascent. Alphabet (GOOG) sold off after the company disclosed financials about specific business units (such as YouTube) for the first time. Investors continued to focus on the coronavirus (with 40,000 confirmed cases and over 900 deaths as of Sunday). China pumped more than $200 billion in liquidity into its economy, and the rate of the spread of the virus fortunately appears to have slowed.

Looking Ahead:

Sixty S&P 500 components are scheduled to report their fourth quarter financial results this week, beginning with Allergan (AGN), DaVita (DVA) and Loews (L) on Monday. Automatic Data Processing (ADP) hosts an innovation day in New York. Tuesday brings financial results from Dominion Energy (D), Under Armour (UA), Hasbro (HAS) and Lyft (LYFT). The Bureau of Labor Statistics reports its Jobs Openings and Labor Turnover Survey for December – economists forecast 6.78 million job openings on the last business day of December, little changed from November. Federal Reserve Chairman Jerome Powell delivers his semiannual Monetary Policy Report to Congress before the House Financial Services Committee. Wednesday is packed with earnings releases, including numbers from Applied Materials (AMAT), Cisco Systems (CSCO), CVS Health (CVS) and Barrick Gold (GOLD). On Thursday, Kraft Heinz (KHC), Pepsico (PEP), Zoetis (ZTS) and Duke Energy (DUK) release financial results. Emerson Electric (EMR) holds its annual investor conference at the New York Stock Exchange. The business week ends with earnings from Newell Brands (NWL) and AstraZeneca (AZN) on Friday. The Census Bureau reports retail sales data for January – economists forecast a 0.3% gain, in line with December’s rise.

The Tufton Capital Team hopes that you have a wonderful week!

Last Week’s Highlights:

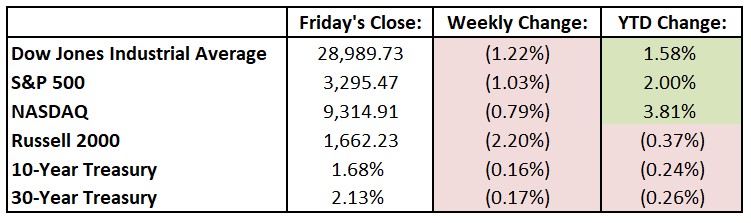

Equities ended the week in the red as American authorities confirmed a second case of the coronavirus in the U.S. and the count of infected patients and deaths rose in China. As of Sunday night, the virus had killed 80, with close to 2100 confirmed cases (including a total of five in the U.S.), while spreading throughout China to neighboring countries. Authorities are especially concerned that the outbreak coincided with the Lunar New Year, when millions of Chinese travel. Earnings season rolled on with largely positive results – numerous companies (and their stocks) performed well, including IBM (IBM), American Express (AXP), Netflix (NFLX), Abbott Laboratories (ABT), and others. However, the coronavirus crisis dampened investors’ moods and market prices. For the week, the Dow Jones Industrial Average (DJIA) fell 358.37 points, or 1.2%, to 28,989.73, while the S&P 500 dropped 1.0% to 3295.47. The tech-heavy NASDAQ lost 0.8%, closing at 9314.91.

Looking Ahead:

This week marks the busiest stretch of fourth-quarter earnings reports, as 132 S&P 500 components release financial results over the next five days. D.R. Horton (DHI), Juniper Network (JNPR) and Whirlpool (WHR) post quarterly numbers on Monday. The Census Bureau releases new home sales data for December – economists forecast a seasonally adjusted annual rate of 728,000 new single-family homes sold, up from November’s 719,000 report. Tuesday is packed with more earnings with releases coming from McCormick (MKC), Lockheed Martin (LMT), Starbucks (SBUX), United Technologies (UTX) and Apple (AAPL). The Conference Board announces its Consumer Confidence Index for January – consensus estimates call for a 128.4 reading, up from December’s 126.5 print. Look for earnings releases Wednesday from AT&T (T), Microsoft (MSFT), Norfolk Southern (NCS), Boeing (BA), T. Rowe Price Group (TROW) and Novartis (NVS). The Federal Open Market Committee (FOMC) announces its monetary-policy decision – the market widely expects the central bank to keep the federal-funds rate unchanged at 1.50%-1.75%. Altria Group (MO), Biogen (BIIB), Coca-Cola (KO) and United Parcel Service (UPS) are among a large group of companies reporting financials on Thursday. The Bank of England releases its monetary-policy decision – futures markets predict a greater-than-50% chance that the central bank will cut its short-term interest rate to 0.50% from 0.75%. Charter Communications (CHTR), Chevron (CVX), Exxon Mobil (XOM) and Honeywell International (HON) report quarterly results on Friday.

The Tufton Capital Team hopes that you have a wonderful week!

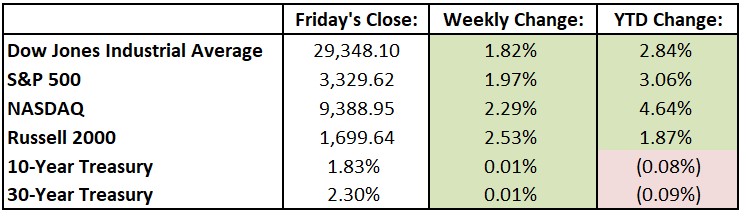

Last Week’s Highlights:

U.S. stocks ended a strong week on a strong note, with the three major equity indexes each rising about 2% last week to record highs. The first wave of companies reporting fourth-quarter earnings was largely positive, as many of the big banks posting strong financial results. Several of these banks’ consumer-related businesses showed robust growth, a positive sign for the overall economy (and market). Alphabet (GOOG) became the fourth U.S. stock to cross the trillion-dollar market-cap line (other members of the trillion-dollar club include fellow tech companies Apple (AAPL), Microsoft (MSFT) and Amazon.com (AMZN)). The U.S. and China signed a phase-one trade deal in Washington – the pact takes some U.S. tariffs on Chinese goods off the table and opens the U.S. to more Chinese purchases. Next up is phase-two which looks to tackle more complicated matters. For the week, the Dow Jones Industrial Average (DJIA) rose 542.33 points, or 1.8%, to 29,348.10, while the S&P 500 advanced 2.0% to 3329.62. The tech-heavy NASDAQ was up 2.3%, closing at 9388.94.

Looking Ahead:

U.S. markets are closed on Monday in observance of Martin Luther King Jr. Day. Fourth-quarter earnings seasons ramps up once markets reopen Tuesday morning, with 43 S&P components releasing financial results through Friday. Capital One Financial (COF), IBM (IBM), Halliburton (HAL) and Netflix (NFLX) release numbers on Tuesday. The World Economic Forum’s 50th annual meeting convenes in Davos, Switzerland. Political and business leaders from around the world will attend, and this year’s theme will be “Stakeholders for a Cohesive and Sustainable World.” On Wednesday, earnings reports include results from Abbott Laboratories (ABT), Johnson & Johnson (JNJ) and Texas Instruments (TXN). The National Association of Realtors reports existing home sales for December – economists forecast a 1.5% rise after declining 1.7% in November. American Airlines Group (AAL), Procter & Gamble (PG) and Southwest Airlines (LUV) report earnings on Thursday. The European Central Bank announces its monetary-policy decision and is widely expected to announce that interest rates will remain steady at negative 0.5%. Friday brings financial results from American Express (AXP) and Air Products & Chemicals (APD). Many markets throughout Asia, including China and South Korea, are closed in observance of the lunar New Year, which falls on Saturday, January 25th.

The Tufton Capital Team hopes that you have a wonderful week!

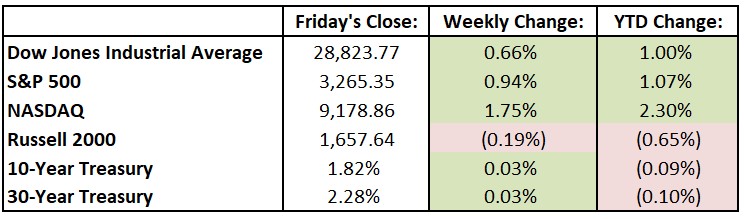

Last Week’s Highlights:

U.S. stocks jumped around last week largely on tensions with Iran and lackluster domestic economic numbers reported later in the week. Equities sold off sharply on Tuesday night on news of an Iranian missile strike. The markets recovered the next morning as it became clear that there had been no casualties and a war was not beginning. By Thursday, the tension in the Middle East was largely forgotten as stocks marched to all-time highs. A lower-than-forecasted December employment number reported Friday led to a selloff, although stocks remained on the positive side for the week. Last week, the Dow Jones Industrial Average (DJIA) rose 188.89 points, or 0.7%, to 28,823.77, while the S&P 500 advanced 0.9% to 3265.35. The tech-heavy NASDAQ was up 1.8%, closing at 9178.86. All three indices are within a half-point of their highest-ever closes.

Looking Ahead:

Fourth-quarter earnings season kicks off this week, with 26 S&P 500 components releasing financial results. Japanese markets are closed on Monday in observance of Coming of Age Day. Banks as usual are among the first to report earnings, and first up are Citigroup (C), JPMorgan Chase (JPM) and Wells Fargo (WFC), as these megabanks release fourth-quarter and full-year 2019 results on Tuesday. The Bureau of Labor Statistics announces the consumer price index (CPI) for December – expectations call for a 2.3% year-over-year rise, following November’s 2.1% increase. Bank of America (BAC), BlackRock (BLK), Goldman Sachs Group (GS) and UnitedHealth Group (UNH) report quarterly earnings on Wednesday. On Thursday, look for more financial results from Bank of New York (BK), CSX (CSX) and Morgan Stanley (MS). The Census Bureau reports retail sales data for December – expectations are for a 0.3% rise, following a 0.2% gain in November. The busy business week concludes with earnings from Citizens Financial Group (CFG), Kansas City Southern (KSU) and State Street (STT) on Friday. The University of Michigan releases its Consumer Sentiment Index for January – economists look for a 99.6 reading, even with December’s print.

The Tufton Capital Team hopes that you have a wonderful week!

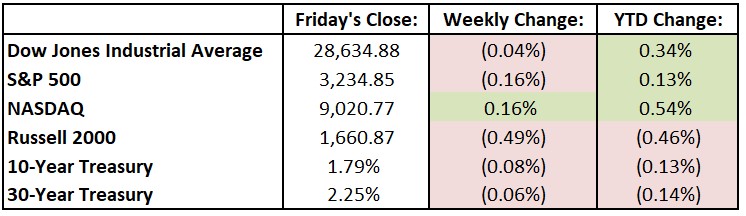

Last Week’s Highlights:

Stocks finished 2019 on Tuesday close to record highs, as the Dow Jones Industrial Average (DJIA) ended the year up 22.3%. The S&P 500 and tech-heavy NASDAQ performed even better last year, finishing up 28.9% and 35.2%, respectively. The new year began with U.S. equities reaching new highs Thursday on reports of China stimulus, then slipped on Friday with the turmoil in the Middle East. For the week, the Dow declined 10.38 points, or 0.04%, to 28,634.88, while the S&P 500 fell 0.2% to 3234.85. The NASDAQ was up 0.2%, closing at 9020.77.

Looking Ahead:

Wall Street returns to its first full week of trading since the holidays began. Cal-Maine Foods (CALM) reports quarterly earnings on Monday. On Tuesday, the Institute for Supply Management releases its Non-Manufacturing Purchasing Managers’ Index for December – consensus estimates call for a 54.5 reading, about even with November’s data. Wednesday brings earnings reports from Bed Bath & Beyond (BBBY), Constellation Brands (STZ) and Walgreens Boots Alliance (WBA). The Federal Reserve reports consumer-credit data – consumer debt is expected to continue its rise to just below the $4.2 trillion level. KB Home (KB), Synnex (SNX) and Acuity Brands (AYI) report financial results on Thursday. The Department of Labor releases initial jobless claims for the week ending on January 4th – the four-week average of claims is 232,500. Infosys (INFY) reports quarterly results on Friday.

The Tufton Capital Team hopes that you have a wonderful week!