The First Quarter of 2018: Coming Back To Earth

By Eric Schopf

The first quarter served as a reminder that the stock market can, in fact, go down. Higher interest rates and global trade tensions collided with a market left vulnerable by the recent surge in share prices and valuation levels. Although the Standard and Poor’s 500 was only down 0.8% for the quarter, it felt much worse because of the nearly 9% retreat from February through March. The drop came after the market was up nearly 7.5% for the first four weeks of January alone. January’s gain was on top of 2017’s 21.8% return and left the market ripe for a pullback. Fixed income securities provided little shelter during the quarter with prices falling and yields rising. The 10-year Treasury moved from 2.43% to 2.74%, while the 3-month Treasury moved from 1.39% to 1.72%.

The political climate has added a layer of uncertainty with trade tensions running high. President Trump would like to reset trade agreements that he thinks are disadvantageous to America. His initial salvo was to impose tariffs on imported steel and aluminum. Although the United States imports steel from countries around the world, the tariffs are aimed primarily at China. The president has also taken aim at Canada and Mexico by expressing his displeasure with the North American Free Trade Agreement (NAFTA). China retaliated by announcing tariffs that primarily target an assortment of agricultural products. Trade talks with Canada and Mexico are ongoing, and no retaliatory measures have been taken.

We would not characterize the current situation as a “trade war” due to the limited scope of the newly-proposed tariffs. Metals and agricultural products are mere pawns in a game with far more important issues at stake. Technological knowledge and intellectual property rights are the kings and queens of the board. We cannot stress enough the importance of free and fair trade. Disruptions in trade policies could have a negative impact on economic growth and corporate profits. So far, the result has been increased volatility in the markets. But we are not ready to hit the panic button yet. The President has established a pattern of taking an aggressive and emphatic stance on important issues. He then backs off a bit as the negotiation process unfolds and he moves on to his next agenda topic. As with any negotiation, there are at least two parties at the table. China’s reaction will obviously impact the outcome of trade negotiations. It is clear to many that the tariffs put in place by China to protect their fledgling economy and key industries are now outdated. They have established themselves as viable producers on the global stage and no longer require the same level of protectionism for support. We believe the current trade disputes will be settled with minimal economic disruption.

Higher interest rates reflect an economy on solid footing. However, rising rates also mark the anticipation of additional interest rate hikes over the balance of the year. The Federal Reserve increased the federal funds target rate to 1.75% in March and two to three more increases are in the offing. The last rate increase was the sixth since the end of 2015. Short-term interest rates are directly impacted by Federal Reserve policy and have moved the most. Longer-term rates reflect economic growth and inflation expectations. The increase in long-term rates has lagged the short end of the yield curve, creating a headwind for stocks. Higher rates have also triggered some concern in the credit markets. Low interest rates provide an inexpensive source of funding for business. However, refunding the debt may become problematic when interest rates rise or when the economy begins to falter and the earnings available for debt service contract.

As the quarter closed, technology-enabled stocks were in the spotlight. Facebook and Alphabet (Google) garnered attention over data privacy issues. Amazon, a favorite target of President Trump, was once again in his cross hairs as he attributed the United States Postal Service’s fiscal deficits to undercharging for package delivery. The drop in value of these three companies has cast a pall over the market since they are three of the largest corporations in the U.S.

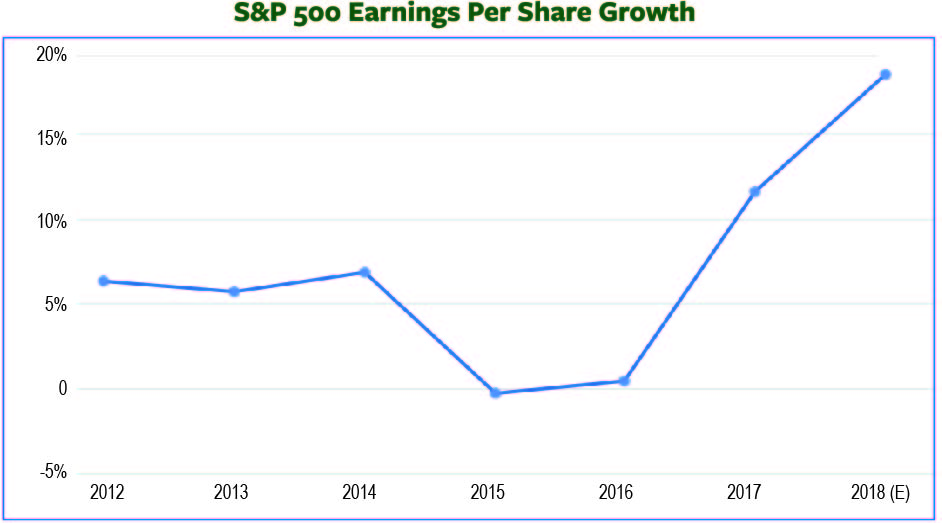

So where do we stand as we enter the second quarter? The economy continues to chug along with the engine stoked by a shot of lower corporate and personal income tax rates. Inflation remains subdued despite a very strong job market. Trade relations are being reassessed, and although there will be winners and losers, we should avoid economy-buckling protectionism. Corporate profits are growing at a healthy clip and dividend increases are being funded with income tax windfalls. The primary concern remains the action of the Federal Reserve in response to a strengthening economy and falling unemployment. The big complication comes from the engine-stoking fiscal policy. Such policy is very unusual for the late stages of a business cycle. Typically, fiscal stimulus is initiated during or following a recession to give the economy a jump start. Monetary policy, that is, the actions of the Federal Reserve to promote maximum employment and stable prices, is being put to the test. Economic growth is determined primarily by the growth in the workforce plus the rate of productivity improvement. For the U.S., this indicates growth potential of around 2%. U.S. economic growth has exceeded expectations and has been closer to 3% due to a cyclical rebound in demand in addition to the fiscal stimulus. Absent the stimulus, the Fed’s job might be finished. However, with the economy running hotter than planned, the concern is that wages will rise and inflation will become a problem, leading to a more hawkish Fed. The Chairman, as well as half of the Federal Reserve Open Market Committee, has been replaced, adding to this uncertainty.

These economic and political concerns are bringing the stock market back down to earth. With a new quarter comes a new set of challenges. We are using the opportunity to find investments to add value to your portfolio.