Last Week’s Highlights:

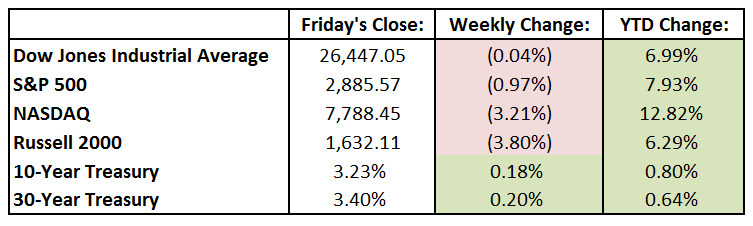

U.S. stocks were lower on the week, as volatility returned along with plenty of news and economic data for investors to digest. After hitting an all-time high early in the week, the Dow Jones Industrial Average (DJIA), along with many other indices, declined largely due to a sudden jump in the 10-year Treasury yield. The yield spiked from 3.055% to 3.227% last week, marking its highest level since May of 2011. As a result, the blue-chip DJIA dropped over 11 points for the week, to 26,447.05, while the S&P 500 fell 1%, to 2885.57. The tech-heavy NASDAQ felt even more pain for the week, dropping 3.2% to 7788.45. Why don’t stocks like these higher interest rates? Aren’t interest rates rising because of solid economic growth, which is a good thing? The answer is yet, BUT this uptick in bond yields brings on concerns that this good economic news may lead the Federal Reserve to tighten more aggressively than has been anticipated. We at Tufton Capital continue to believe that strong earnings and economic growth justifies this rising rate environment, and equities can still perform well despite the increased volatility.

Looking Ahead:

The U.S bond market is closed on Monday in observance of Columbus Day. Markets are closed in Canada for Thanksgiving and in Japan for Health and Sports Day. Proctor & Gamble (PG) holds its annual shareholder meeting in Cincinnati on Tuesday, and the National Federation of Independent Businesses reports its Small Business Optimism Index for September. On Wednesday, the Bureau of Labor Statistics releases its producer price index for September. Honeywell International (HON) hosts an investor conference in New York that day, where it will discuss its spinoff of Resideo Technologies. Thursday brings earnings reports from Commerce Bancshares (CBSH) and Walgreen Boots Alliance (WBA). We’ll also see plenty of economic reports that day, including the consumer price index for September and August’s real average weekly earnings results. The week ends with three of the four largest U.S. banks reporting their third quarter results: Citigroup (C), J.P. Morgan Chase (JPM) and Wells Fargo (WFC) all report results on Friday.

The Tufton Capital Team hopes that you have a wonderful week!

Last Week’s Highlights:

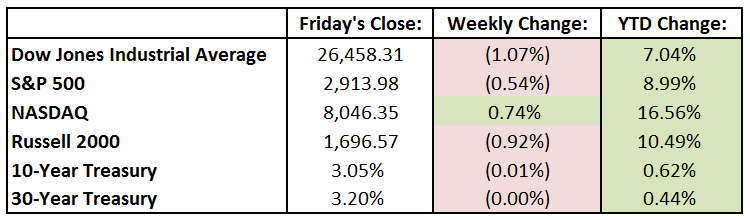

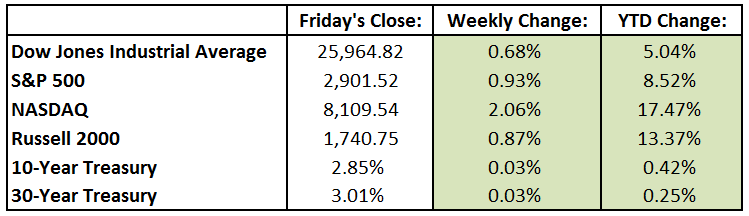

Most of the major US indices were down last week as tariff talks and the Federal Reserve weighed on strong quarterly performance. The Dow Jones Industrial Average was down 1.1% while the S&P 500 was down 0.5%. On the other hand, the technology heavy Nasdaq rose 0.75%. For the quarter, the three major indices posted their best quarterly performance since 2013. On the economic front, the biggest headline news was the Federal Reserve raising interest rates another quarter of 1%. The Federal Funds Rate now stands in a range of 2% to 2.25%. Housing was also in focus last week. New Home Sales were reported at 629,000 for the month of August, which was slightly below Wall Street’s estimate, but 21,000 higher than the number reported in July. Home Prices, as evidenced by the S&P/Case-Shiller Index, rose 0.1% for the month of July. Lastly, Durable Good Orders surged 4.5% in the month of August, beating the Wall Street estimate of 1.9%.

Looking Ahead:

This week, stocks are off to a strong start as the US, Canada, and Mexico agreed on a new trade agreement that will replace the current North American Free Trade Agreement (NAFTA). Jobs will also be in focus this week starting with the ADP Employment Survey on Wednesday. On Friday, investors will gain further insight on the job market with Average Hourly Earnings, Nonfarm Payrolls, and the Unemployment Rate all being released by the Bureau of Labor Statistics. With the end of the calendar quarter, many companies will be preparing for quarterly earnings calls in the next coming weeks.

The Tufton Capital Team hopes that you have a wonderful week!

Last Week’s Highlights:

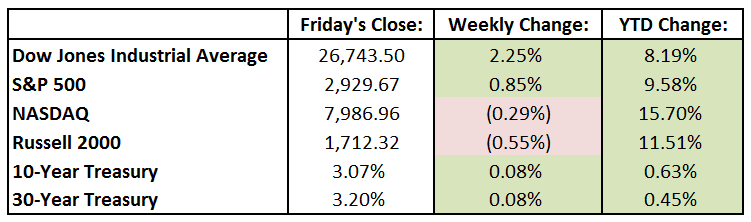

U.S. large-cap stocks edged higher Friday, finishing off their strongest two-week stretch since February. This recent strength in domestic equities reflects that inflation- and trade-related anxieties that have affected the markets in recent months may be abating. For the week, the Dow Jones Industrial Average gained 589 points, or 2.3%, to 26,743.50 – a record close. The S&P 500 rose 0.8% last week to 2929.67, narrowly missing a record of its own. It was an unusually weak week for the FAANG stocks (Facebook (FB), Amazon (AMZN), Apple (AAPL), Netflix (NFLX), Alphabet (GOOGL)), as the tech-heavy NASDAQ dropped 0.3%, to 7886.96. There was an unusual move last week between the U.S. dollar and the 10-year treasury yield, as the two usually move up (or down) together. Last week, however, the yield on the 10-year rose to 3.068% (its sixth-highest close of the year), while the U.S. Dollar index fell 0.8%, its second consecutive weekly decline.

Looking Ahead:

The trade war heats up on Monday, as U.S. tariffs of $200 billion on Chinese goods are expected to take effect. China is also expected to impose tariffs of $60 billion on U.S. goods. The Federal Reserve meeting begins on Tuesday, and we’ll see earnings out of Nike (NKE) and comments from the General Mills (GIS) annual shareholder meeting in Minneapolis. On Wednesday, the Fed will announce its interest-rate policy decision: consensus estimates anticipate that the Fed will raise the federal-funds rate by a quarter percentage point, to 2%-2.25%. On Thursday, the Census Board reports durable-goods orders for August, and the National Association of Realtors releases its Pending Home Sales Index for last month. We’ll see earnings reports from McCormick (MKC), Accenture (ACN) and Conagra Brands (CAG) that day as well. The week ends with the Bureau of Economic Analysis’s release of personal income and outlays for August, as well as earnings reports from BlackBerry (BB) and Vail Resorts (MTN). The New York Film Festival officially opens on Friday.

The Tufton Capital Team hopes that you have a wonderful week!

Last Week’s Highlights:

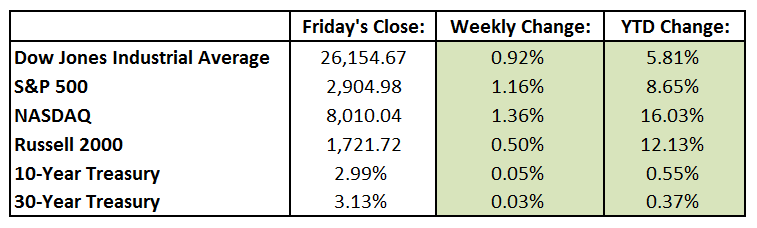

The major indices rose last week as investors expected that the U.S. and China were going to resume trade talks. The tech-heavy Nasdaq led the way, with Microsoft (MSFT) contributing the most to the index’s return by gaining 1.36%. A plethora of economic data was released last week. The Producer Price Index (excluding food and energy) fell 0.10% month over month, showing that the cost of producing goods declined. The Consumer Price Index (excluding food and energy) rose 0.1% month-over-month and 2.2% year-over-over. This rate of inflation is near the Federal Reserve’s target, signaling that the Fed will likely raise interest rates again later this month.

Looking Ahead:

While Monday does not bring market moving economic data, the housing market will be in focus throughout the remainder of the week. On Wednesday, information on Building Permits will be released for August. Wall Street is estimating that 1.3 million building permits were issued, on par with the 1.3 million building permits issued in July. Existing Home Sales information will be released on Thursday. Consensus estimates are for 5.4 million homes sales for the month of August. On the earnings front, there will not be many releases, as the third calendar quarter is coming to an end.

Have a wonderful week!

Last Week’s Highlights:

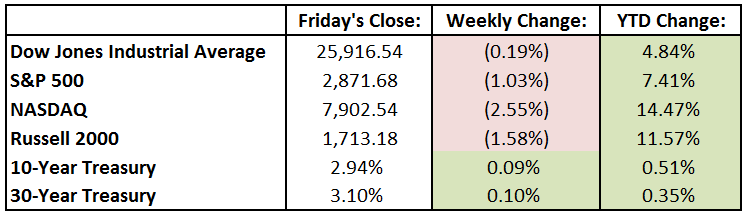

Technology stocks were hit last week, largely due to Wednesday’s congressional testimonies by senior executives of two leading social media companies (Facebook (FB), Twitter (TWTR)). Additionally, the Department of Justice said it would meet with state attorneys general on what it called the “stifling” of voices online by social media. As a result, the tech-heavy NASDAQ fell 2.55% for the week to 7902.54. August’s solid jobs report was released on Friday, showing that the economy added more than 200,000 jobs and that wages grew at the fastest pace since 2009. However, this strong report failed to overcome pressure of escalating trade tensions: the Dow Jones Industrial Average slipped 0.19% for the week, and the S&P 500 fell 1.03%, to 2871.68. Amazon.com (AMZN) briefly joined Apple (APPL) last week with a trillion-dollar-plus market capitalization on Tuesday, before slipping back to $995 billion. The pair are the first two U.S. companies to join the trillion-dollar club. Congratulations to Novak Djokovic and Naomi Osaka for winning tennis’s U.S Open – it was his third victory in the New York event and her first.

Looking Ahead:

Monday starts the first day of Rosh Hashanah, and AT&T will host an investor conference to discuss the recent acquisition of Time Warner. Tuesday marks the 17th anniversary of the 9/11 terrorist attacks. On Wednesday, Apple (APPL) hosts its annual Gather Round event, where the company is expected to unveil new iPhone models and a redesigned Apple Watch, among other products. Wednesday will be a busy day on the economics front, as we’ll hear from the Bureau of Labor Statistics on the August producer price index as well as the Federal Reserve, which will release its sixth of eight beige-book surveys for 2018. Thursday brings the consumer price index report for August and earnings reports from Adobe System (ADBE) and Kroger (KR). And on Friday, we’ll see more economic news, including the August retail sales report and the Consumer Sentiment survey for September.

Have a wonderful week!

Last Week’s Highlights:

Last week, the major indices trekked higher as an agreement with Mexico signaled that new regulations could replace the North American Free Trade Agreement (NAFTA). The Dow Jones Industrial Average rose 0.7%, while the S&P 500 increased 0.9% and the Nasdaq jumped 2.1%. The S&P 500 and tech-heavy Nasdaq both reached all-time highs – surpassing their records set this past January. For the month of August, the Nasdaq surged 5.9%, the S&P 500 had a total return of 3.3% and the Dow Jones Industrial Average lagged with a total return of 2.6%. Of the 3.3% for S&P 500, Apple was the largest contributor representing 24% of the index’s return.

Looking Ahead:

This week, investors will be focused on the Trade Balance report, to be released at 8:30 AM Wednesday. Wall Street is expecting a deficit of $50 billion for the month of July. On Thursday, data on the Durable Good Orders for July, as well Unit Labor Costs for the 2nd Quarter, will be released. Consensus estimates forecast that Durable Good Orders declined 1.7% in July and Unit Labor Costs declined 0.9%, respectively. Friday is “Jobs Day” as a plethora of information is released regarding the Labor Market. Wall Street is estimating that the economy added 190,000 Nonfarm Payroll Jobs in the month of August. The Unemployment Rate is expected to decline from 3.9% to 3.8% and Hourly Earnings are expected to rise 0.3% month over month.

Last Week’s Highlights:

After almost seven months since its January 26th top, the S&P 500 once again hit a new all-time high. The S&P is now up over 7% for 2018, while the Dow Jones Industrial Average and NASDAQ are up 4.33% and 15.1% YTD, respectively. Stocks posted their largest gains on Friday, following Federal Reserve Chair Powell’s speech in Jackson Hole, where he noted that while the committee’s measure of inflation has moved near its 2% target, an inflation overshoot or an overheating economy does not seem likely. This will likely keep the Federal Reserve on pace to raise short-term interest rates at a measured pace, hopefully helping extend the bull market.

Looking Ahead:

It’s the (unofficial) last week of summer and traditionally a slow one for Wall Street. After the U.S. Open tennis tournament kicks off on Monday, we’ll see earnings from Tiffany & Company (TIF) and Best Buy (BBY) on Tuesday. Wednesday will bring the GDP revision data, pending home sales, and earnings reports from Salesforce (CRM) and Dick’s Sporting Goods (DKS). On Thursday, we’ll get economic readings on personal income, consumer spending and core inflation. Warren Buffett will celebrate his 88th birthday that day, and we’ll get financial results from Dollar Tree (DLTR), Campbell Soup (CPB) and Abercrombie & Fitch (ANF). Friday will round out the week with the consumer sentiment index.

All of us at Tufton Capital wish you an enjoyable and safe Labor Day weekend!

Last Week’s Highlights:

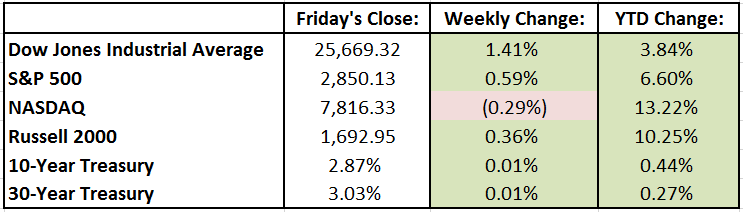

Last week, the Dow Jones led the major indices with a 1.41% increase week-over-week. Walmart (WMT) helped lead the index higher rising 8.5% after beating Wall Street estimates for both sales and earnings-per-share. The Arkansas-based company also raised their sales guidance for the year. Nielsen Holdings (NLSN) was the largest gainer in the S&P 500 increasing nearly 20% week-over-week. Activist Elliott Management took a stake in the information and data management company with intention of pushing the Board-of-Directors for a strategic review of the business. In economic news, retail sales beat Wall Street estimates rising 0.5% month-over-month versus a consensus estimate of 0.2%. Housing starts came in slightly below consensus at 1.17 million.

Looking Ahead:

This week, investors will get further results from the retail sector with Kohl’s (KSS) and TJX (TJX) both reporting quarterly results on Tuesday. Target (TGT) and Lowe’s (LOW) will report before the opening bell on Wednesday with Williams Sonoma (WSM) reporting after the closing bell. On Thursday, investors will hear from L Brands (LB), The Gap (GPS) and The Children’s Place (PLCE). On the economic front, housing will continue to be in focus with the release of July Existing Home Sales on Wednesday morning. July New Home Sales as well as July Building Permits will be released on Thursday Morning.

Last Week’s Highlights:

U.S large-cap stocks finished lower on the week, their first weekly decline since the end of June. The DJIA fell 149 points on the week (0.6%), while the S&P 500 declined 0.2% to 2833.28. The NASDAQ eked out a gain of 0.3%. Weighing on equities were worries of financial and currency turmoil in Turkey as well as continued tariff talks between the U.S. and China. Turkey’s lira tumbled 14% on Friday, as a standoff over an imprisoned U.S. pastor led to President Trump doubling tariffs on that nation’s steel and aluminum exports. From there, the strain in Turkey spread to other markets.

We also saw some active Tweeting last week, but this time it wasn’t just from the Oval Office. Elon Musk of Tesla Inc. (TSLA) informed his Twitter followers on Tuesday that he’d like to take his electronic car maker private for $420 a share. Tesla’s board is weighing the deal, and Musk claimed that the necessary funding has been secured, largely from the Saudi Arabian sovereign wealth fund.

Looking Ahead:

Earnings season continues to wind down this week, as we’ll see results from fewer than 3% of companies in the S&P 500 reporting their second-quarter numbers. Earnings that Tufton’s research team will be especially focused on this week include Home Depot’s (HD) results on Tuesday, Cisco (CSCO) and Macy (M) numbers on Wednesday, and Nordstrom (JWN) and Walmart (WMT) on Thursday. Important economic reports this week include retail sales (Wednesday), housing starts (Thursday), and the leading economic index to wrap up the week. And of course we can’t forget the very important “Left Handers Day” celebrated on Monday and “Men’s Grooming Day” on Friday!

Last Week’s Highlights:

Labor data was bittersweet, as the labor force added fewer jobs than expected during July but revisions to earlier months’ data brought the unemployment rate down below 4% again. The $1,000,000,000,000 question was finally answered on Thursday when Apple became the first company in history to hit trillion-dollar market cap. Indices were slightly up across the board, with the NASDAQ leading the way.

Looking Ahead:

In the revolving door of economic indicators, inflation is up next. The producer and consumer price indexes will be released toward the end of the week, giving us a hint at how well the Fed’s rate hikes have been keeping the economy from overheating. A fairly stellar earnings season continues to wind down, with most companies having already reported strong second quarter results. Media takes the spotlight this week, as investors will put Disney, Viacom, and Fox under the microscope in a shifting landscape of established names.

What’s On Our Minds:

As sure as the sun will rise in the east and set in the west, the stock market will go up and it will go down. Rather than getting caught up in these daily fluctuations, the investment professionals at Tufton Capital believe that a long-term buy and hold strategy is the safest and smartest way to build wealth. A disciplined adherence to this philosophy has proven time and time again to return exponential gains on invested capital, regardless of how the market is feeling on any given day.

Cultivating Your Portfolio

The term “buy and hold” doesn’t mean investing and forgetting about your portfolio for the next 20 years. There are ways to cultivate and prune your portfolio while still maintaining a long-haul investing strategy. For instance, if a company you invest in changes fundamentally, you may not want to continue owning that security. If the overall market changes dramatically, as it has in the past, you may actually benefit from selling an investment or group of investments. Finally, changing goals as you get closer to retirement may warrant a more conservative portfolio.

Bad Markets

The typical investor is tempted to get out of a bad market by selling when prices are low, which is a poor strategy. The economy fluctuates between good and bad all the time, and those who constantly buy and sell will be hit the hardest in a bad economy. By holding on to your investments, you’ll be better able to ride out a down market, especially if your portfolio is diversified.

Taxes and Fees

Frequent trading results in higher fees, so long haul-investors pay less while fees eat up much of a day trader’s profits. Additionally, short-term gains are taxed at a higher rate than long-term gains. Even if you have the fortune of timing the market successfully, your profits will be diminished by taxes and fees.

Investing for the long-haul is the best investing strategy for the majority of investors because it not only ensures modest gains but is also less likely to yield major losses. A long-haul investment strategy is based on informed, careful decision making and patience.

Last Week’s Highlights:

The Bureau of Economic Analysis released its GDP estimate for the second quarter of 2018, placing growth at 4.1% — the highest since 2014. Though there are a few one-time factors that have brought that number up, such as soybean and aircraft exporters rushing product out before retaliatory tariffs went into effect, increased spending by both businesses and consumers was the main driver. Indices flipped the familiar script last week, with the Dow posting the biggest increase and the NASDAQ losing just over 1%. The tech-heavy composite index came down from record highs after weak earnings reports and cautious guidance from Twitter, Intel, and Facebook, with the latter having the biggest single-day loss in value in the history of the stock market. Each of these tech giants experienced double-digit percentage losses in share price as spooked investors fled the technology sector. In a win for free trade, President Trump and the head of the European Commission agreed to working toward a zero-tariff solution, temporarily sidelining auto import taxes until a more detailed deal can be worked out.

Looking Ahead:

Earnings season is finally beginning to wind down, hopefully bringing some level-headedness to the markets. It’s not over yet, though, as big names like Apple, Caterpillar, DowDuPont, Procter & Gamble, Volkswagen, and Kraft Heinz report this week. The Federal Reserve, the Bank of England, and the Bank of Japan all have meetings before taking most of August off, making the next few days some of the most significant of the season in terms of macroeconomic policy news. Consumer Confidence and Employment reports are due by the end of the week, which, coupled with last week’s GDP numbers, should inform the Fed’s decision whether to raise rates again soon.