Company Spotlight: Nordstrom, Inc. (Ticker: JWN)

by Scott Murphy

It is a well-known fact that Nordstrom (Ticker: JWN) is the retailer with the greatest return policy in the industry: if you are not happy with your purchase, return it for a no-questions-asked refund. This laser focus on the customer experience is what separates Nordstrom from its competitors and inspires the customer loyalty that is the envy of the retailing world. With its headquarters in Seattle, Washington, it is currently operating 315 stores in the U.S. and Canada. These include 121 full-line stores and 194 Nordstrom Racks located in 38 states with good prospects for store growth in underserved regions of the country.

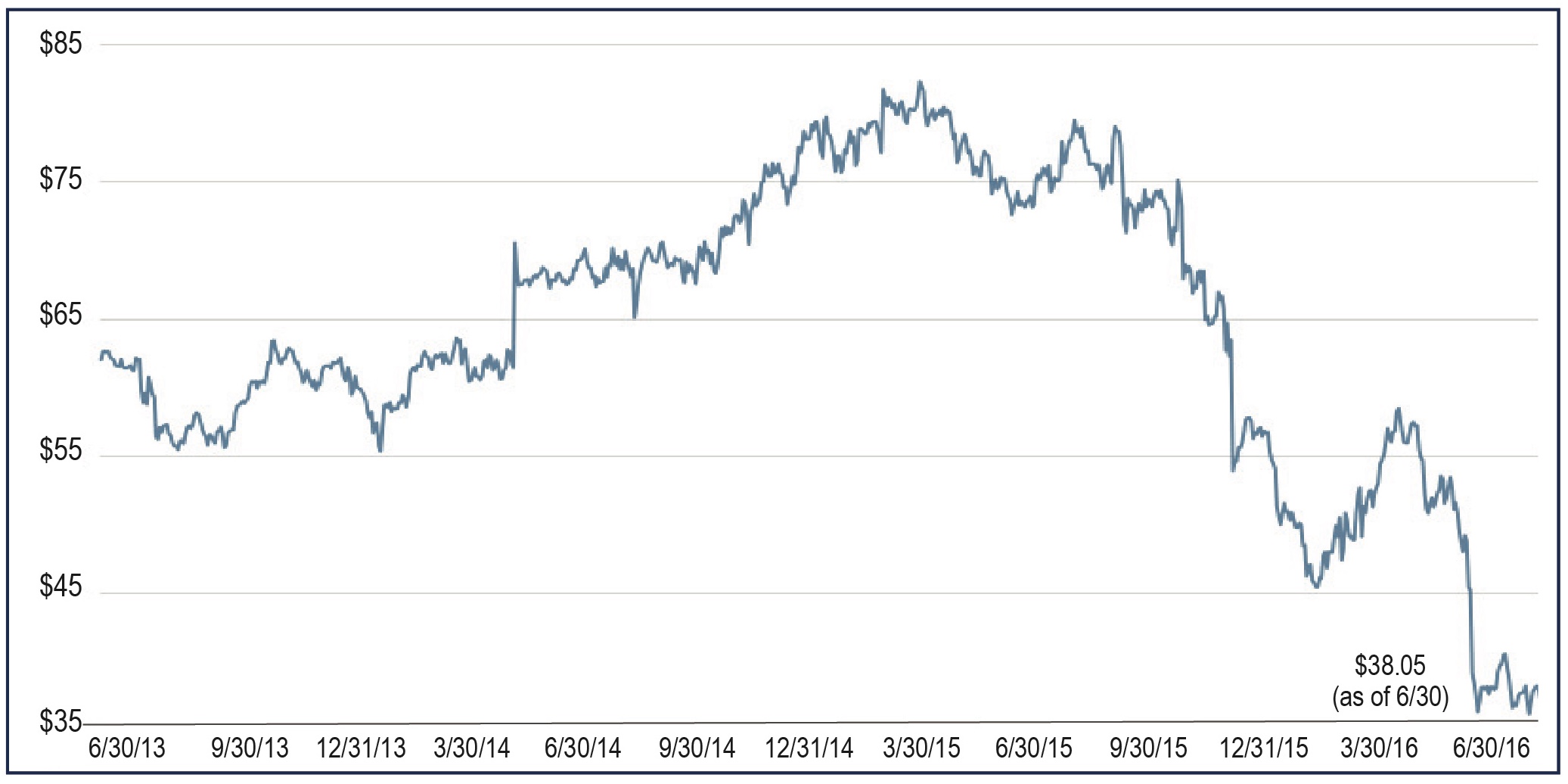

The stock price has fallen 20% year to date due to a significant reduction in its sales forecast and expected earnings per share for 2016. Nordstrom certainly isn’t alone in this consumer-led stock selloff, and of those in its industry that have sold off, Nordstrom retains a leading position. Management is pulling back store openings and will cut its corporate staff by 10% in order to better position the company for rosier times. As value-oriented investors, we will continue to monitor this investment and stay patient. We believe our original thesis is still intact, and more time is needed for the underlying business of this great company to recover.

We still feel Nordstrom is a solid company and will trade higher as the industry conditions improve. The company has a strong balance sheet, is selling at five-year lows using Price/Earnings and Price/Cash Flow metrics and has a generous 4% dividend yield. Sometimes it takes patience for a great company to work out to be a great investment. Brick and mortar retailers are not “in fashion” right now on Wall Street, but we believe that fact means a good value for our clients.

Nordstrom (JWN) Price Performance