The Fourth Quarter of 2016: Well That Changed Everything

by Eric Schopf

Donald Trump’s victory and his subsequent tweets announcing fiscal policy initiatives dominated the fourth quarter. The Standard and Poor’s 500 had posted modest gains for the year heading into the election. However, from November 8th through the close of the year, the market tacked on over 5%, bringing the year’s total return to 12%. Not bad reflecting back to mid-February when the market was down over 10%.

President Trump’s platform of fiscal stimulus has resonated with equity investors. More spending, lower tax rates, and fewer regulations are a stark contrast to the restrictive policies in place since the financial crisis. With a Republican-controlled Congress, many of the financial goals should be attainable. Early Cabinet appointees, which have included many experts from the corporate world, are proof that Mr. Trump is quite serious about achieving his goals.

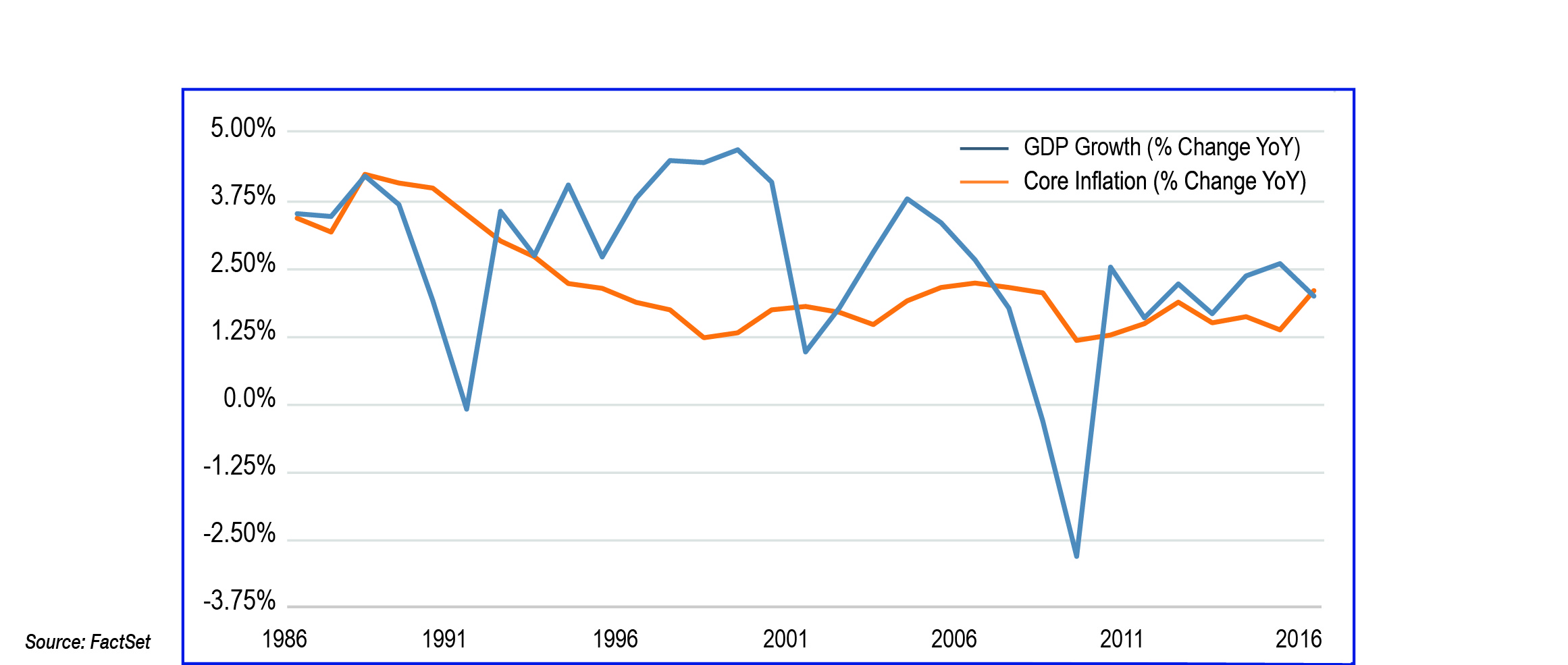

The Federal Reserve has stated on many occasions that monetary policy alone wasn’t enough to revive the economy. The Fed encouraged greater fiscal action by lawmakers. Mr. Trump has delivered. The Fed’s response to more robust economic growth could be the difference between success and failure. Although the Fed did increase the Federal Funds rate by 0.25% in December, the rate hike is just the second in the past eight years. Interest rates remain low, reflecting anemic economic growth and inflation levels running consistently below the 2% target. Letting inflation run hot for a period may allow the economy to build momentum to withstand higher interest rates.

U.S. Core Inflation vs. Real GDP Growth

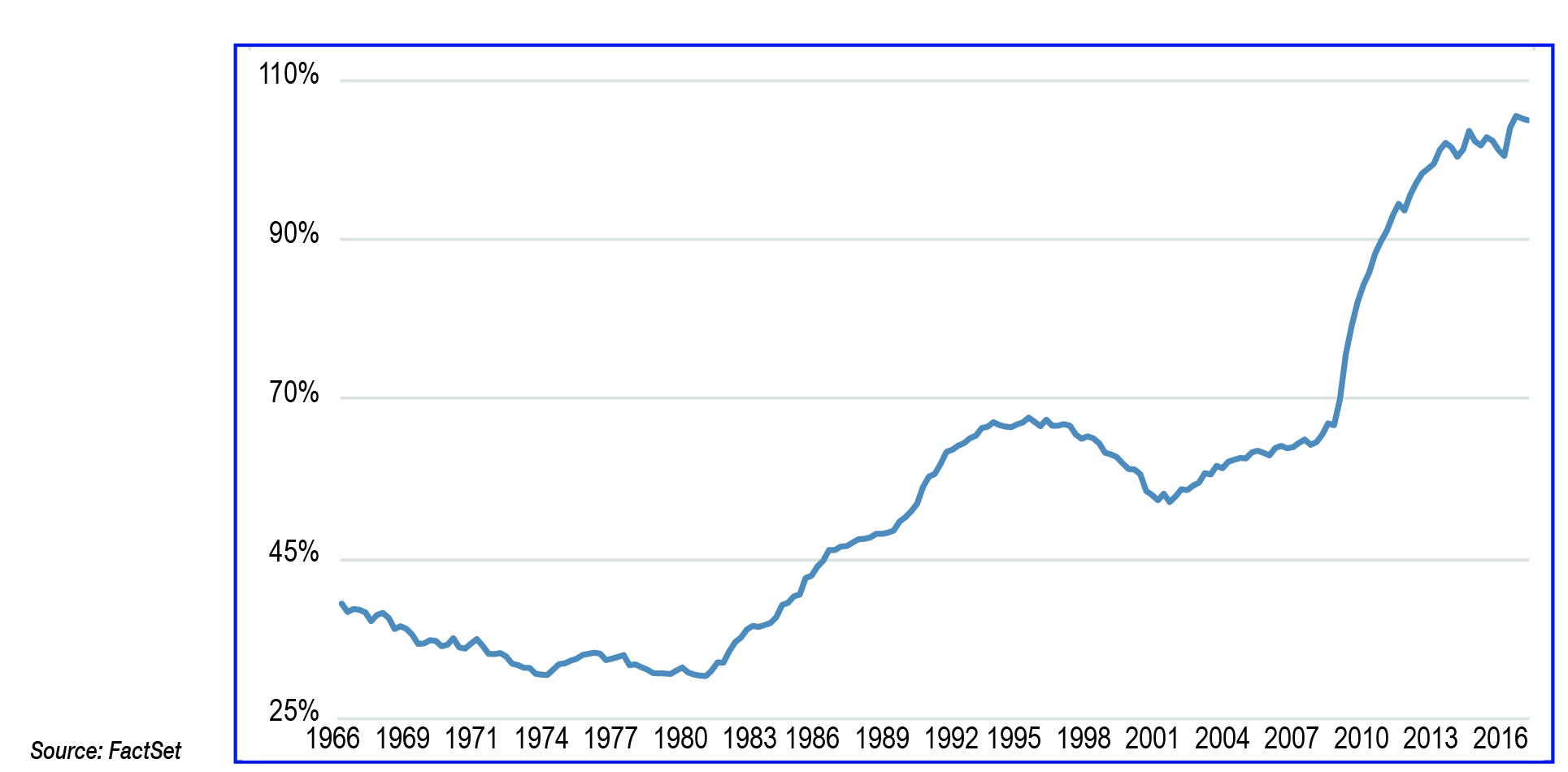

Future market returns will depend on two key variables. First, what incremental growth will be provided by the new policies? Second, how and when will the Federal Reserve respond to stronger growth and higher inflation? Before answering these important questions, we must first understand the limitations of lower tax revenue and greater spending. The U.S. national debt now stands at roughly $20 trillion, or 106% of gross national product. The debt/GDP ratio is at record levels (discounting periods of war). Entitlement programs, Medicare/Medicaid and Social Security, combined with defense spending, account for approximately 78% of total spending, leaving little room for financial maneuvering.

Various sources have estimated that the fiscal policy could add anywhere between 0.25% and 1.8% to economic growth. While the improvement would be welcomed, the estimates fall short of the 4% economic growth trumpeted by Mr. Trump. The U.S. has not posted a 4% annual GDP growth since 1999. However, just reaching 3% growth could provide the perfect blend of growth. This rate would likely not ignite inflation and would thus avoid the commensurate response of higher interest rates.

Interest rates have also had a dramatic move since the election. The rate on the 10-year U.S. Treasury moved from 1.78% prior to the election to 2.48% by year-end. Higher rates reflect expectations for better economic growth and the need for the Treasury to issue more debt to finance anticipated spending. Interest rates on one-month to five-year Treasury issues are at multi-year highs in anticipation of further Fed tightening. Municipal bonds did not fare well in the quarter as the prospect for lower individual tax rates reduces the appeal of tax-exempt income. Higher interest rates will come as a relief to investors who have watched yields continuously fall from the peak reached in 1981.

An improving economy coupled with an accommodative Fed can provide a powerful environment for the equity markets. Soaring consumer confidence adds a strong third rail. However, there are two potential hurdles in this rosy scenario. The first is the uncertainty surrounding U.S. trade policy. Mr. Trump has talked tough on trade, continuing his campaign theme of staunching the exodus of U.S. jobs. Intervention in current trade pacts, regardless of whether they are free or fair, may lead to retaliatory actions. Trade restrictions or other protectionist measures would have a profound impact on the economy and the fortunes of many multi-national companies. Second, the continuing strength of the U.S. Dollar presents challenges to corporate profits. Revenue and profit generated overseas is translated from foreign currency to U.S. Dollars for financial statements. Weak foreign currencies lead to fewer U.S. Dollars being reported and a possible reduction in earnings. The Mexican Peso, Canadian Dollar, Chinese Yuan, Japanese Yen, British Pound, and the Euro are all trading at multi-year lows versus the U.S. Dollar.

As we begin the New Year, we are confronted with risk and uncertainty. The strong post-election response of the stock and bond markets has quickly discounted the potential positive results of policies that aren’t even in place. However, risk and uncertainty present opportunity. We will continue to maintain our value discipline in identifying high quality investments that, in our opinion, are trading at temporarily depressed levels. We appreciate your support and confidence as we remain focused and dedicated to achieving favorable results, regardless of the market environment.

U.S. Debt as a Percentage of U.S. GDP