The Weekly View (4/17/17)

What’s On Our Minds:

Tufton Capital is committed to helping our clients implement financial plans that will help keep them on track during their retirement years. By establishing a financial plan, you will determine how your investment assets will fund your financial needs, wants, and wishes. Seeing that saving enough for retirement is the most important part of the planning process, review our 10 Tips for Saving for Retirement Below.

Start now: It’s a simple fact that the earlier you begin saving for retirement, the more time your money has to earn interest and grow. If you’ve put off saving until your 30s or later, make up for lost time now by stashing away 10 to 15 percent of your salary.

Plan your retirement needs: If you want to retire at 55 and travel the globe or work for as long as you can but stick close to home, how much money you need to retire is unique to you. Rather than relying on figures that suggest you’ll need 80 percent of your pre-retirement income to live comfortably later in life, talk with your spouse and portfolio manager to settle on an amount to save that’s tailored to you.

Learn about and contribute to your employer’s plan: If your employer offers a tax-sheltered plan, contribute at least enough to get the employer match. Your employer can provide you with a summary plan description, which recaps your plan and vesting eligibility, as well as an individual benefits statement.

Consider saving “on the side”: If you don’t have access to an employer-based plan, contributing to a traditional or Roth IRA allows you to get similar tax benefits for your retirement savings. Even if you do contribute to an employer-based plan, an IRA can supplement those savings.

Make saving as easy as possible: Eliminate the need to move money from one account to another by setting a monthly savings goal and automating a deposit to that amount. By making savings routine, you are more likely to see your retirement nest egg grow. To help boost your regular savings, funnel any extra cash windfalls, such as from a bonus or inheritance, directly to your retirement savings.

Increase savings as your near retirement: Your income will likely rise with age and experience, so it makes sense to save more as you earn more. After age 50, you will also be eligible for catch-up contributions, which allow you to contribute beyond the set limit. For 401(k)s, you can contribute an extra $6,000, while for IRAs you can contribute an extra $1,000.

Be an active participant in your retirement plan: Automating your retirement savings and amount doesn’t mean you should “set it and forget it.” Examine your quarterly statements to ensure you are on track to meet your goals. Can you afford to contribute more? Are your investments still appropriate? Do you need to lower your exposure to risk? By taking active control now, you take control of creating the best retirement lifestyle possible.

Decide on your Social Security strategy: Social Security benefits may be available at age 62, but up until age 70, your retirement benefit will increase by a fixed rate (based on your year of birth) each year you delay retirement. Waiting means you may be able to take advantage of some extra cash. If you are married, you may also be able to receive spousal benefits, which boost the amount you and your spouse receive in Social Security as a couple. To learn more, visit www.socialsecurity.gov.

Be a savvy investor: It’s important to be smart about not only the amount you save but also how you save. Keep tabs on how your investment accounts are performing and keep in touch with your portfolio manager. The more intentional you are about how your assets are invested, the more secure you can feel about them.

Don’t touch your savings until retirement: Dipping into your retirement savings is a last resort. In addition to harsh penalties, you lose principal, which in turn depletes interest earnings and tax benefits. Also, if you switch jobs, rollover your retirement account rather than “cashing out.” Preserving your retirement savings may be difficult when funds are tight, but will benefit you when you truly need it most.

Last Week’s Highlights:

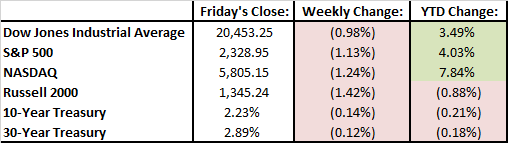

In an abbreviated week of trading due to Friday’s holiday, stocks declined roughly 1% in the face of global tensions with Syria, Russia, and North Korea. Because of the international drama, we saw a dip in bond yields as investors “flew to safety” and put more money into U.S. Treasuries. Along with geopolitical pressure, earnings season kicked off and investors weighed earnings reports from large U.S. banks. Wells Fargo shares fell 3.3% after reporting a slowdown in their mortgage banking business. Warren Buffet’s Berkshire Hathaway said it was forced to sell more than 7 million shares of Well Fargo’s stock in order to keep their ownership stake in the bank below 10%. The move to cut its stake keeps Berkshire from having to become a bank holding company.

Looking Ahead:

Investors will be examining first quarter earnings reports this week and working through anymore geopolitical turmoil that may arise. Netflix and United Airlines report their first quarter results on Monday. On Tuesday, we will hear from Goldman Sachs, Bank of America, and IBM. On Friday, Samsung will release their new Galaxy S8 mobile phone.