The Weekly View (8/10/20)

Last Week’s Highlights:

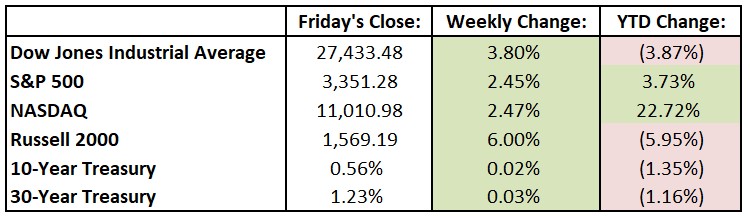

U.S. equities were higher last week across various indexes, as stocks were helped by encouraging employment numbers. Nonfarm payroll employment climbed by a stronger-than-expected 1.8 million in July. That was lower, however, than the 4.8 million and 2.7 million totals for June and May, respectively. Earning season continued with 82% of S&P components exceeding analyst forecasts so far this quarter, well above the 71% average during the past four quarters. Corporate America has held up better than many expectations according to these relatively upbeat results. For the week, the Dow Jones Industrial Average (DJIA) rallied 1,005.16 points, or 3.8%, to 27,433.48, while the S&P 500 rose 2.5% to 3351.28. The NASDAQ gained 2.5%, closing at 11,010.

Looking Ahead:

Second-quarter earnings season continues as a number of S&P 500 components release results this week beginning with Duke Energy (DUK), Marriott International (MAR) and Simon Property Group (SPG) on Monday. The Bureau of Labor Statistics (BLS) reports its Job Openings and Labor Turnover Survey for June – economists call for 5.1 million job openings on the last business day of June, down from 5.4 million in May. Sysco (SYY) announces financial results on Tuesday. The BLS releases the producer price index (PPI) for July, which is expected to rise 0.2% month over month after falling 0.2% in June. Wednesday brings earnings releases from Cisco Systems (CSCO) and Lyft (LYFT). The BLS releases the consumer price (CPI) data for July – consensus estimates call for a 0.7% rise from last year’s number. Applied Materials (AMAT), Baidu (BIDU) and Brookfield Asset Management (BAM) report financials on Thursday. On Friday, the Census Bureau announces retail sales data for July – economists forecast a 2% monthly rise in retail sales.

All of us at Tufton Capital wish you a safe and healthy week.